– Green Finance And Carbon Markets – Financial Services")

To print this article, all you need is to be registered or login on Mondaq.com.

2023 REGULATORY MAINLINE REVIEW

1. Significant regulatory breakthroughs in peak carbon and

carbon neutrality; interplay of legislative initiatives and changes

respond to market needs

In 2023, a number of regulations, documents or consultation

drafts in relation to climate change and “Carbon Peaking and

Carbon Neutrality” were introduced to provide legislative

support for sustainable development. The measures taken were:

- firstly, the legislative hierarchy has been improved. After

continuous refinement of the draft in 2023, the Interim

Regulation on the Administration of Carbon Emission Trading

was formally adopted at the executive meeting of the State Council

on January 5, 2024. This is the first domestic administrative

regulation for administration of carbon emission trading and

addresses the issues that had arisen from existing regulations and

rules for carbon emissions trading (i.e. the goals of regulating

trading activities, guaranteeing trading data quality and punishing

illegal behaviors were only somewhat erratically supervised by the

relatively low-level (i.e. not central level) legislative hierarchy

of such existing regulations and rules). - secondly, on October 19, 2023, the long-awaited Measures

for the Administration of Voluntary Greenhouse Gas Emission

Reduction Trading (For Trial Implementation) (the

“New CCER Regulation“) was officially

released, as the basis and guideline for the systems of the

restarted national greenhouse gas voluntary emissions reduction

trading market (the “CCER Market“). - thirdly, in April 2023, the NDRC revised the Measures for

the Energy Conservation Examination of Fixed-Asset Investment

Projects, emphasizing the integration of energy conservation

with the goal of “Carbon Peaking and Carbon Neutrality”;

on March 16, 2023, the NDRC issued a consultation draft of the

revised Guiding Catalog of Green Industries, which is

expected to be formally promulgated and implemented in 2024;

moreover, the NDRC issued a revised version of the Catalogue

for Guiding Industry Restructuring at the end of 2023, which

became effective on February 1, 2024 and emphasized the energy

saving, carbon emission reduction and green transition.

The promulgation or update of the foregoing regulations and

documents not only responds to the development and practice of the

goal of “Carbon Peaking and Carbon Neutrality”, but also

provides strong support for achievement of such goal.

According to the legislative plan released by the Standing

Committee of the 14th National People’s Congress in September

2023, the legislation with aims of addressing climate change and

achieving Carbon Peaking and Carbon Neutrality is still considered

as a legislative project which lacks certain legislative conditions

and requires further research. Therefore, the enactment of laws to

be promulgated by the National People’s Congress such as

Climate Change Law, Carbon Emission Reduction Law or

Carbon Financial Inclusion Law may take more time; while

the revisions to be made on some other laws such as the Energy

Law, the Renewable Energy Law, and the Marine

Environmental Protection Law have been put on the agenda, with

the expectation of incorporating the applicable contents to address

climate change and ensure the realization of the goal of

“Carbon Peaking and Carbon Neutrality”.

2. “1+N” Policy Framework Upgraded; Transition

Finance and Inclusive Carbon Financeng

The policies and guidelines issued by applicable authorities and

central and local governments remain as the important tools for

addressing climate change and achieving the goal of “Carbon

Peaking and Carbon Neutrality”.

In 2023, under the established “1+N” policy framework

for Carbon Peaking and Carbon Neutrality, the supporting policies

were further refined by the appropriate regulatory authorities

:

- following the promulgation of provincial-level implementation

plans for Carbon Peaking in many provinces in 2022, some

sector-specific Carbon Peaking implementation plans were further

introduced in 2023 in some provinces/municipalities (e.g. those

issued in Hebei, Inner Mongolia, Zhejiang, Fujian, Chongqing,

Tibet, Shaanxi and Qinghai, and the Carbon Peaking implementation

plans for the urban-and-rural construction sector issued in Hebei,

Shanxi, Jiangsu, Fujian, Shandong, Henan, Hubei, Hunan, Chongqing,

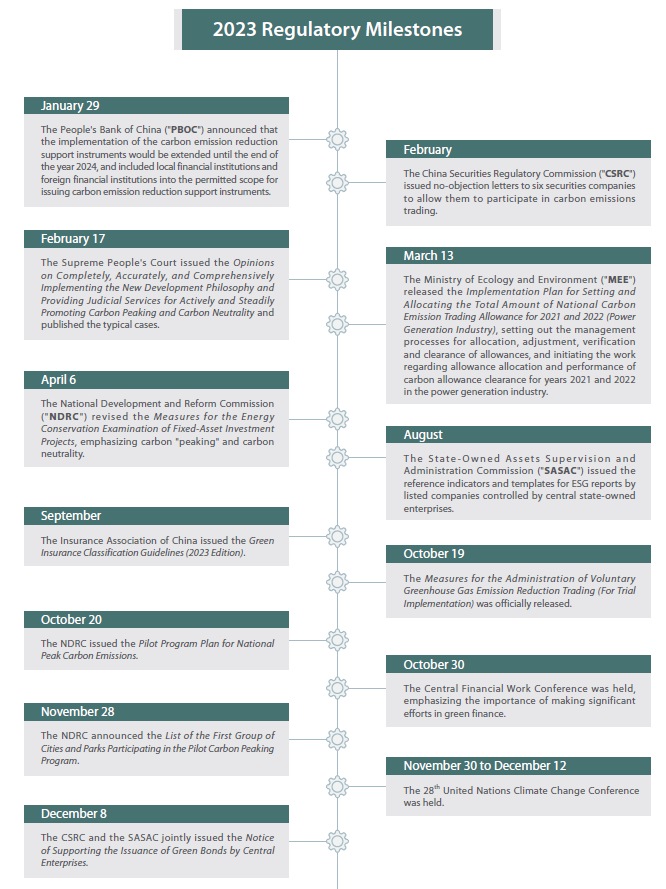

Guizhou, Qinghai and Xinjiang); - at the end of October, the NDRC issued the Pilot Program

Plan for National Peak Carbon Emissions, proposing that

“financial institutions shall be encouraged to support the

construction of cities and industrial parks implementing the peak

carbon dioxide emissions pilot program, comprehensively use

financial tools such as green credit, green bonds and green funds,

and increase support for relevant green and low-carbon projects in

a market-oriented manner”, and also announced the list of

first group of national “carbon peaking” pilots at the

end of November; - on December 8, the CSRC and the SASAC jointly issued the

Notice of Supporting the Issuance of Green Bonds by Central

Enterprises, guiding and supporting the central enterprises to

raise funds through the green bonds market, and boosting the

development of the green industry.

Climate finance is an important policy instrument in achieving

the goal of “Carbon Peaking and Carbon Neutrality”. After

the jointly announced list of climate finance pilots (i.e. a total

of 23 approved pilot cities/areas) by MEE and eight other

applicable authorities in August 2022, these pilot cities/areas

have issued a series of policies to promote the implementation of

the pilot programs, the majority of which have already established

the climate finance project databases and platforms to match

governments, banks and enterprises in 2023. Certain pilots such as

Nansha District in Guangzhou, have put in place specific and

quantitative financial incentive policies for enterprises, projects

and talented persons.

In addition to climate finance, the promulgation of G20

Transition Finance Framework issued in the end of 2022, which

was led by the PBOC (as one of the co-chairs of the G20 Sustainable

Finance Working Group), marks the first international consensus

reached between major countries on the development of transition

finance. In March 2023, the government work report of the 14th

National People’s Congress emphasized the importance of the

role of finance in bringing about green transition. At the end of

March, the vice-governor of the PBOC was also quoted as saying that

the PBOC would actively promote the promulgation and implementation

of transition finance standards as soon as practicable. The PBOC

has taken the lead in drafting transition finance standards for

four industries (i.e. the industries of coal and electricity, iron

and steel, building materials and agriculture) and would publish

consultation drafts in due course. The finance work plans and green

finance policies by local regulatory authorities also mentioned the

promotion of the linkage between green finance and transition

finance. As for the market practice, the Bank of China issued the

first steel transition finance bond (the first in the world) on

October 12 with all the funds raised being used to support the

green transition projects of the iron and steel industry in Hebei

province.

In 2023, the local governments actively explored policies of

carbon financial inclusion. For example:

- the Key Tasks List for the 2023 Municipal Government Work

Report of Beijing proposed improving incentives for carbon

financial inclusion and incorporating low-carbon travel scenarios

such as replacing fuel-powered motor vehicles with electric ones

into the scope of carbon financial inclusion incentives; - several work plans (or drafts) to create a carbon financial

inclusion system were published in some provinces, such as Shandong

and Anhui, proposing the establishment of personal carbon accounts

and offset channels for certified emission reduction of carbon

financial inclusion, the formation of expert committees for carbon

financial inclusion, and the development of appropriate

institutional standards and methodologies; - the authorities in Hainan and Guangzhou issued

implementation/administration measures on carbon financial

inclusion; - the Cooperation Framework Agreement for the Construction of

the Carbon Financial Inclusion Platform in the Greater Bay

Area was entered into by two organizations in Guangdong

Province and the Macau Special Administrative Region, aiming to

cooperate in the exploration of carbon financial inclusion; - the Shanghai Municipal Bureau of Ecology and Environment issued

the Administration Measures for Carbon Financial Inclusion in

Shanghai Municipality (for Trial Implementation) in November,

and also published a series of ancillary guidelines such as the

development and application guidelines for methodologies, and

carbon financial inclusion projects and carbon emission reduction

scenarios, as well as the guidelines on the use of carbon financial

inclusion credits. These efforts have laid the foundation for

establishing a local carbon financial inclusion system.

3. New Green Finance Policies Open Up to New Participants and

Products

In 2023, more regulations and policies related to green finance

were implemented:

- with the expiration of the one-year transition period in May

2023 as provided in the Guidelines on Green Finance for the

Banking Industry and the Insurance Industry, the banking and

insurance institutions have set up and refined their internal green

finance-related management systems and processes; - in September, the Insurance Association of China issued the

Green Insurance Classification Guidelines (2023 Edition),

which provides self-regulation in three aspects: green insurance

products; green investment of insurance funds; and green operation

of insurance companies; - The central and local regulators issued policies to encourage

and support the local development of green finance and carbon

finance. For example, (i) the former CBIRC, the CSRC and the State

Administration of Foreign Exchange (“SAFE”) and some

other authorities, together with the Guangdong Province Government,

jointly issued the policy to support the development of green

finance in Guangdong-Macao In-Depth Cooperation Zone in Hengqin and

Qianhai Shenzhen-Hong Kong Modern Service Industry Cooperation Zone

and strengthen the green finance cooperation in the GBA; (ii) the

financial regulators in a number of provinces/municipalities such

as Shanghai, Beijing, Tianjin, and Hebei introduced policies to

actively promote the healthy development of the local green finance

market; and (iii) the Shandong Province Government launched a

three-year action plan to promote the development of carbon

finance.

It is expected that the green finance related regulations will

be further revised and refined under the existing institutional

framework in the coming period.

With the ongoing development of the domestic sustainable finance

market, the policies have become increasingly open to attract

various types of market participants to participate in sustainable

finance. For example, at the end of January 2023, the PBOC not only

decided to extend the effective period for the implementation of

the carbon emission reduction support instruments to the end of

2024, but also extended the scope of institutions permitted to

issue such instruments to include local financial institutions and

foreign financial institutions, as well as national financial

institutions, aiming at encouraging more financial institutions to

participate in the financing of such areas as clean energy, energy

conservation and environmental protection, and carbon emission

reduction technologies by using monetary policy tools.

In terms of the carbon market, in February 2023, six securities

company announced that they had received no-objection letters from

the CSRC to allow them to participate on their own account in

carbon emissions trading. To date, eight securities company have

successfully obtained such official no-objection letters and are

permitted to carry out proprietary trading in the carbon emissions

trading market.

While the market for single green-themed financial products has

become more mature, there is more activity when it comes to

exploring new products which combine greenness with something else.

For example, the first domestic green and energy supply dual-themed

asset-backed security (“ABS”) was issued in April 2023,

followed by the issuance of the first domestic green and low-carbon

transition-linked ABS in June. Green financial products have also

been developed to cover sectors such as rural revitalization: for

example, in March, the Agricultural Bank of China took the lead in

underwriting the first domestic carbon emission right asset-backed

bond with four themes (i.e. carbon neutrality, carbon assets, rural

revitalization and old revolutionary base areas). Currently,

innovations in the green finance market are still mainly about

investments, i.e., incorporating green investment targets and

sustainable elements such as green and/or low-carbon performance

indicators into more traditional and mature transaction and product

structures. We expect that innovations in product structures will

gradually emerge as the market deepens its understanding of green

finance in the future.

4. Carbon Quotas: Stable Nationwide Market with Continued

Regional Growth

In terms of the “top-level” legal framework, the

Interim Regulation on the Administration of Carbon Emission

Trading (“Interim Regulation“) was

formally adopted at the executive meeting of the State Council on

January 5, 2024, laying out the basis of the institutional

framework for administration of the carbon emission trading in the

mandatory National Carbon Market. The Interim Regulation clarified

the trading system of the national carbon market for the first time

in the form of the administrative regulation. This addresses

defects in the existing regulations and rules (such as the

Measures for the Administration of Carbon Emissions Trading

(for Trial Implementation)) but also coordinates the efforts

of multiple applicable authorities (including ecological and

environmental departments) to promote the development of the

trading and management of carbon emissions trading. Another

highlight of the Interim Regulation is that compared with the

existing regulations, it strengthens the processes for punishing

those acting illegally (such as falsifying carbon emission data) in

order to safeguard quality of carbon emission data.

The second performance period of the national carbon emissions

trading market (the “National Carbon

Market“) has finished. On July 17, the General Office

of the MEE issued the Notice on the Work Related to the

Clearance of Carbon Emission Allowances for the Years 2021 and 2022

in the National Carbon Market, according to which the second

performance period of the National Carbon Market was two years

(i.e. the relevant key emission entities were required to complete

the settlement and clearance of carbon emission allowance allocated

respectively for the years of 2021 and 2022 before December 31,

2023). The policies for the second performance period will

introduce differentiated allowance allocation and performance and

also introduces flexibility when it comes to allocations of carbon

emission allowances, to make adjustments for those with allocation

shortfalls or facing clearance difficulties.

Regional carbon markets continued to play a role in 2023. Some

regional carbon markets have made significant adjustments, for

example lowering the entry threshold for market participants,

expanding the scope of industries affected and introducing

innovative products. The current version of the Interim Regulation

does not require existing regional carbon markets to be

incorporated into the National Carbon Market. These regional carbon

markets must be aligned with the Interim Regulation. Although

regional carbon markets will gradually be phased out as the

national carbon market takes over, they can still serve as useful

policy testing grounds.

5. Voluntary Carbon Market: CCER Market Relaunched with

Regulatory Framework Beginning to Take Shape

The voluntary greenhouse gas emission reduction trading market

(“CCER Market“) and the National Carbon

Market complement each other. Together, they are the two basic

pillars of the carbon market in China. On October 19, 2023, the

long-awaited New CCER Regulation was formally released, serving as

the foundation and guidance for the regulatory framework of the

relaunched CCER Market. Based on that, the applicable regulatory

authorities issued ancillary rules (such as the four methodologies

for CCER projects in the categories of forestation carbon sinks,

mangrove vegetation, grid-connected solar thermal power generation,

and grid-connected offshore wind power generation; the guidelines

for the design and implementation of CCER projects; the

registration and trading settlement rules for CCER projects; and

the implementation rules of approval and carbon emission reduction

verification of CCER projects). All of this means that the

preliminary regulatory framework of the national CCER Market has

been set up.

Benefiting from the relaunch of the CCER Market, loan products

linked to the registration or development progress of CCER projects

have emerged. The Industrial Bank issued the first loan product

linked to approval and verification of CCER projects. So far as the

carbon sink market is concerned, the CPC Central Committee and the

State Council proposed the inclusion of certified voluntary

emission reductions from carbon sinks in relation to conservation

of water and soil and forest resources in the voluntary carbon

market in the Opinions on Strengthening the Water and Soil

Conservation Work in the New Era and the Reform Program on

Deepening the Collective Forest Right System. This points to

the integration of the carbon sink market and carbon market.

6. Towards a Standardized System for Carbon Reduction; Carbon

Footprint Regulatory Framework Taking Shape

In April 2023, the Standardization Administration and other 10

departments jointly issued the Guideline for Establishing a

System of Standards for Carbon Peaking and Carbon Neutrality,

which sets out a series of standardization construction work and

objectives related to “Carbon Peaking and Carbon

Neutrality” (including green finance product and service

standards and green finance evaluation and assessment standards).

In July, the National Technical Committee of Carbon Peaking and

Carbon Neutrality Measurement and its technical sub-committees were

set up, and one of their core tasks is to strengthen the

requirements for measuring data on carbon emissions and carbon

monitoring, and to research and formulate technical specifications.

The objective is to ensure robust measurement of carbon trading and

carbon verification. Standards for environmental assessment, carbon

emissions and energy consumption for various industries are

gradually being formulated and released.

In 2023, the applicable authorities outlined the framework for

how the carbon footprint in China is managed. On October 12, 2023,

the State Administration for Market Regulation issued the

Implementation Opinions of the State Administration for Market

Regulation on Coordinating the Use of Quality Certification to

Serve the Work of Achieving Carbon Dioxide Peaking and Carbon

Neutrality, which requires that carbon identification

certification (such as the product carbon footprints) to be carried

out gradually. On October 20, the NDRC issued the Pilot Program

Plan for National Peak Carbon Emissions, proposing to explore

the ancillary policies such as product carbon footprint management.

On November 13, the NDRC and other four departments jointly issued

the document guiding the establishment of the domestic product

carbon footprint management system, (Opinions on Accelerating

the Establishment of a Product Carbon Footprint Management

System). The document clarifies the overall requirements, key

tasks, safeguard measures and organizational implementation

requirements for enhancing the management level of key product

carbon footprint in China, builds up the overall framework of the

product carbon footprint management system, and expressly supports

enterprises to voluntarily carry out product carbon footprint

certification, as required by the market. In terms of general

standards, in November 2023, the applicable departments issued the

consultation draft of the recommended national standard of

Requirements and Guidelines for Quantification on the

Greenhouse Gases Carbon Footprint of Products. In addition,

the China National Accreditation Service for Conformity Assessment

issued the consultation draft of the Accreditation Scheme for

Product Carbon Footprint Validation and Verification Bodies on

January 4, 2024.

7. ESG Disclosure Brought in Line with International

Standards

In recent years, although China’s companies have made

progress in their ESG development and the scope and quality of ESG

disclosure, the lack of unified, standardized and localized rules

has long been a pain point hindering their development of ESG. In

response to the requirements of the Work Plan for Improving the

Quality of Listed Companies Controlled by Central SOEs issued

by the SASAC of the State Council in 2022, the General Office of

the SASAC issued the Notice on Research on the Preparation of

ESG Special Reports of Listed Companies Controlled by Central

SOEs in August 2023, in order to facilitate the preparation of

ESG special reports by listed companies controlled by central

state-owned enterprises (SOEs). This is the first time that the

Chinese government has provided specific and systematic

interpretations of ESG disclosure standards. The appendix includes

the Reference Indicator System for ESG Special Reports of

Listed Companies Controlled by Central SOEs and the

Reference Template for ESG Special Reports of Listed Companies

Controlled by Central SOEs, which provide basic references for

state-owned listed companies in the preparation of ESG special

reports. The selected ESG indicators align with the international

common standards such as GRI, TCFD, SDGs (United Nations

Sustainable Development Goals) and ISO, and are conceptually

consistent with the new ISSB standards.

In terms of industries, the Insurance Association of China

issued the Guideline on Disclosure of Environmental, Social and

Governance (ESG) Information for Insurance Institutions on

December 13, 2023. The guideline is the first domestic industrial

self-regulatory document focusing on the framework and content of

ESG disclosure in the insurance sector, which combines China’s

particular circumstances with international advanced practice, with

special emphasis on disclosure requirements related to rural

revitalization and financial inclusion. The Beijing Private Equity

Association released the General Principles for Disclosure of

Sustainable Investment Information for Private Investment Fund

Managers on September 4, 2023, which became the world’s

first group standard in the private investment fund sector in terms

of sustainable investment/ESG.

8. Judicial Practice In Step with the Times

As the goal of “Carbon Peaking and Carbon Neutrality”

continues to advance, the judicial practice in China related to

green finance and the carbon market is also keeping up. In February

2023, the Supreme People’s Court issued the Opinions on

Completely, Accurately, and Comprehensively Implementing the New

Development Philosophy and Providing Judicial Services for Actively

and Steadily Promoting Carbon Peaking and Carbon Neutrality.

This document requires China’s judicial systems to

“adjudicate the cases related to energy conservation and

emission reduction, low-carbon technologies, carbon trading, green

finance and other related matters in accordance with the law; to

promote climate change mitigation and adaptation”, emphasizes

the “establishment and improvement of the trial mechanism for

carbon-related cases”, and puts forward specific opinions on

the trial methods and key points of the 17 types of cases closely

related to the goal of “Carbon Peaking and Carbon

Neutrality” (such as the cases relating to economic and social

green transition, industrial restructuring, low-carbon energy

system construction, and carbon market trading). On the same day,

the Supreme People’s Court also released new types of cases in

relation to environmental resource trials in recent years,

involving (among others) environmental infringement cases arising

from greenhouse gas emissions, disputes over carbon emission

allowances transfer contracts, disputes over CCER technical service

contracts, enforcement of administrative penalties for the

settlement of carbon emission allowances, and enforcement of carbon

emission allowances. Such cases reflect the active exploration and

practice of the judicial system on the protection of new types of

environmental rights and interests, and will provide important

reference for the subsequent relevant cases across the country.

In terms of the criminal cases, the Interpretation of

Several Issues Concerning the Application of Law in Handling

Criminal Cases Involving Environmental Pollution issued by the

Supreme People’s Court and the Supreme People’s

Procuratorate on August 8, 2023, mentioned the issue of criminal

liability for the authenticity of information related to carbon

emissions, and stated that “where any employee of an

intermediary organization charged with the duty of inspection and

testing of greenhouse gas emissions, or preparation or inspection

of emission reports intentionally provides a false supporting

document” may be liable for the crime of providing false

supporting documents.

So far as enforcement goes, in September 2023, China’s first

judicial case connected with CCER was completed in Sichuan

province. The case marked the first attempt to extend the judicial

enforcement of carbon assets to voluntary carbon emission

reduction, based on the previous enforcement cases related to

carbon emission allowances. The effectiveness of pledging carbon

assets such as carbon emission allowances and CCER has long been a

major concern preventing financial institutions from participating

in carbon financial transactions and developing related products.

Although the reasons for the enforcement of the abovementioned CCER

were not disclosed publicly, this case not only provides useful

experience for the enforcement of carbon assets in the future, but

also boosts market confidence in the liquidity and enforceability

of CCER in the context of the relaunch of the CCER market. It

should also provide a judicial basis for the further development of

the financial business of carbon asset pledge by Chinese financial

institutions in the future.

2024 REGULATORY OUTLOOK

1. With the Regulatory Framework in Place, Detailed Regulations

Will Follow

The promulgation of the Interim Regulation fills the gap in the

high-level legislation on carbon emission trading. We expect that

the applicable authorities will engage in the formulation and

updates of applicable ancillary regulations, measures, standards

and other specific rules (e.g., the coordination process between

the authorities, mechanisms for integrating with the green power

system, the rules related to data quality, the formulation of lists

of key emission entities in specific industries, the allocation and

settlement of carbon emission allowances, the rules for statistical

accounting of greenhouse gas emission data, and the rules for

submission and verification of annual emission reports, and so on),

and further consolidate the institutional framework content of

carbon market under the regulatory framework of the Interim

Regulation .

Although local regulatory authorities are actively exploring

carbon financial inclusion policies, currently no national-level

policy for carbon financial inclusion exists. On August 31, 2023,

the MEE published its Reply to Proposal No. 5859 of the First

Session of the 14th National People’s Congress, to which,

regarding the proposal to formulate the Carbon Financial Inclusion

Promotion Law (Draft) and set up the pilots of carbon financial

inclusion, the MEE replied that “it would collaborate with the

other relevant authorities to conduct researches on the

standardized construction, operation and management of carbon

financial inclusion system, in conjunction with the construction of

the greenhouse gas voluntary emission reduction trading market, and

provide useful guidance for the healthy development of local carbon

financial inclusion systems”.

With respect to the establishment of ancillary rules and

standards of carbon financial inclusion, the MEE said that it would

apply the international standard ISO 14067:2018 (i.e.

Greenhouse gases — Carbon footprint of products —

Requirements and guidelines for quantification) as the common

basic standard, and would work with relevant authorities to improve

the measurement and standard systems for “Carbon Peaking and

Carbon Neutrality”, and conduct in-depth studies about the

unified carbon financial inclusion platform and the necessity and

feasibility of setting up a national carbon financial inclusion

management and operation institution. In the Opinions of the

CPC Central Committee and the State Council on Comprehensively

Promoting the Construction of Beautiful China issued on

January 11, 2024, there is explicit mention for the first time of

“the exploration of establishing of public participation

mechanisms such as Carbon Financial Inclusion” in such a

central level policy. We therefore expect that the top regulatory

framework on carbon financial inclusion will be introduced at some

point.

2. Expansion of the National Carbon Market and Regulatory

Innovation On Course

Although the current National Carbon Market only covers the

power generation industry, we fully expect the industry coverage of

the National Carbon Market to expand. The regulatory authorities

have made this clear through frequent announcements. On October 27,

2023, Xia Yingxian, the head of the Department of Climate Change of

the MEE, mentioned in a press conference that the next step is to

include more eligible industries into the National Carbon Market.

The MEE carries out annual verification of annual carbon emission

accounting reports for industries such as petrochemicals,

chemicals, building materials, iron and steel, non-ferrous metals,

paper-making, civil aviation and other industries and will

prioritize the inclusion of industries that contribute

significantly to achieving the goal of “Carbon Peaking and

Carbon Neutrality”, have overcapacity, exhibit significant

potential for pollution reduction and carbon reduction synergy, and

have good data quality foundations. In November 2023, Zhao Yingmin,

the vice-minister of the MEE, also publicly stated the intention to

“actively and prudently” include more high-carbon

industries in the National Carbon Market.

Also noteworthy is the approach being taken which involves

enterprises bidding for carbon emission allowances. Since 2015,

pilot regional carbon markets have been trying to organize paid

bidding for carbon emission allowances. The regulatory provisions

on paid allocation of carbon emission allowances have evolved from

the previous provision of “paid allocation may be introduced

in due time” as set out in the Measures for the

Administration of Carbon Emissions Trading (for Trial

Implementation) to the current provision of “a method

combining free with paid allocation will be gradually

promoted” as provided in the Interim Regulation. In December

2023, a seminar on paid allocation of carbon emission allocation in

carbon market was held in Beijing, in which more than 30 experts

from the MEE’s Department of Climate Change, universities and

research institutes, exchanges, certification agencies, and

industries (such as power generation, iron and steel,

petrochemicals, building materials, and nonferrous metals)

discussed the necessity, urgency and feasibility of paid allocation

of carbon emission allowances, design of paid allocation schemes,

and the raising and use of paid allocation revenues, among other

topics. This may lead to the development of a paid allocation

scheme for carbon emission allowances in the National Carbon Market

in the near future.

3. Carbon Markets to Gradually Link Up with Other Green Energy

Regimes and Policy Tools

With the development of the carbon market, the connection

between the carbon market and other green resource framework and

policy tools is gradually happening. In September 2023, the Central

Committee of the Communist Party of China and the State Council

issued the Reform Program on Deepening the Collective Forest

Right System, which emphasizes the connection between the

reform of China’s collective forest rights and the green

finance and the carbon market. The document not only proposes

giving full play to the leading role of green finance, studying the

inclusion of eligible forest rights trading services and deep

processing of forest products into the scope of green finance, and

increasing financial support, but also mentions the possibilities

of forestry carbon credit, supporting qualified forestry carbon

sink projects to be developed into greenhouse gas voluntary

emission reduction projects and to participate in market trading,

and the creation of an ecological protection compensation system

reflecting the value of carbon sinks. Although forestry carbon

credits have not yet been included in the trading products of the

National Carbon Market or include allowance for offset by key

emission entities, we will watch out for integration of forestry

carbon credits with green finance, carbon financial products and

market mechanisms before too long.

The connection between the green power market, the carbon market

and the green finance market is also worth watching. In early

December 2023, Hubei Province took the lead in trying out a trading

scheme that links the electricity, carbon and finance markets. In

this scheme, enterprises can obtain low-interest green loans by

pledging carbon emission allowances and using the funds to purchase

green electricity, which in turn can be used to offset a certain

amount of carbon emission allowances. In 2023, policies and

programs for the connection between green electricity and the

carbon market were issued in Beijing, Tianjin and Shanghai.

Although these policies are currently only piloted in certain

enterprises with limited coverage, they serve as a good

demonstration of how the electricity and carbon markets can work

together.

4. Unified ESG Disclosure Standards to Spur Regulation of ESG

Rating Agencies

Although the establishment of unified ESG disclosure standards

has been a long-standing topic, the release of the Reference

Indicator System for ESG Special Reports of Listed Companies

Controlled by Central SOEs and the Reference Template for

ESG Special Reports of Listed Companies Controlled by Central

SOEs by the General Office of the SASAC signifies a solid

first step taken by top-level regulators towards applicable unified

ESG disclosure standards for enterprises in different industries

and sectors. Although these documents still only apply in scope to

state-owned enterprises, with the accumulation of practical

experience and feedback, it is certain that the authorities will

further introduce ESG disclosure standards with a broader scope of

application.

In addition to the lack of unified actions and disclosure

standards, the inconsistency and lack of transparency in the

evaluation standards of ESG rating agencies is also one of the

reasons that makes it difficult for enterprises to engage in ESG

development. Some other jurisdictions have already explored the

regulation of ESG rating agencies in 2023. For example, the HM

Treasury in the UK has launched a consultation on regulations to

bring all ESG-related data and rating products (regardless of

whether they are identified as ESG ratings) under the oversight of

the Financial Conduct Authority (“FCA“);

the European Commission has also followed suit by proposing

regulation rules for ESG rating agencies that are roughly

consistent with the EU’s Benchmarks Regulation

(“BMR“) system; and the Monetary

Authority of Singapore (“MAS“) released

an official version of Code of Conduct for ESG Ratings and Data

Product Providers on December 7 and encourages ESG rating

agencies to disclose how much their voluntary codes of conduct are

being adopted locally. Given that the ESG-related regulatory

framework for domestic enterprises has taken shape, at least in

preliminary form, we expect that domestic regulatory authorities

will explore the regulatory rules for ESG rating agencies in due

course.

5. Perservering with Globalization of Standards amidst

International Cooperation and Challenges

In 2023, China continued to promote international cooperation on

sustainable finance. For example, the Monetary Authority of

Singapore (“MAS“) and the PBOC jointly

set up the China-Singapore Green Finance Taskforce

(“GFTF“); China and the United States,

despite complicated international politics and diplomacy, still

carried out the Track II Dialogue on Climate Finance and exchanges

on climate change legislation, and after two meetings of the

China-U.S. special envoy for climate change, China and the U.S.

jointly issued the Sunnylands Statement on Enhancing

Cooperation to Address the Climate Crisis and launched the

Working Group on Enhancing Climate Action in the 2020s in

November 2023. Following the 28th session of the Conference of the

Parties (“COP 28“) to the UN Framework

Convention on Climate Change (“UNFCCC“),

the Chinese government stated that it would continue to firmly

promote green and sustainable development and “do its best

part” in the global response to climate change. We also expect

China will be more active in the arena of international cooperation

on sustainable finance policies, standards and market

practices.

In addition, as the international influence of sustainable

finance, carbon emission reduction, and ESG concepts grows

stronger, the impact of foreign legislation on domestic enterprises

is increasingly significant. For example, the EU’s Carbon

Border Adjustment Mechanism (CBAM), known as the “carbon

tariff”, took effect as EU law in May 2023, which means that

before the end of the transition period (i.e. the end of 2025),

Chinese enterprises may face additional carbon tariffs if they are

unable to effectively control the carbon emissions of their

products – leading to a possible decline in the competitiveness of

their products in the EU market. The environmental and

sustainability requirements in the new version of the

Regulation Concerning Batteries and Waste Batteries in EU,

which entered into force in July 2023, also brings additional costs

and challenges to the export of products from China’s booming

new energy enterprises. We will watch out to see whether China will

introduce response policies and countermeasures.

The release of the New CCER Regulation and the relaunch of the

CCER Market have left room for speculation about cross-border

carbon trading, and businesses are looking forward to the

authorities issuing policies to allow the mutual conversion between

projects under other greenhouse gas emission reduction programs and

CCER projects. During the COP28, an official from the MEE expressed

“the emphasis on the importance of the internationalization of

the carbon market for accelerating global climate action, and the

willingness to explore feasible implementation paths and policy

tools to promote greenhouse gas emission reduction jointly with

various carbon market mechanisms”, but also emphasized that

“engaging in cross-border carbon trading involves aligning

with applicable international rules, which will have an impact on

China’s fulfilment of its goal of nationally determined

contributions (NDCs) and requires coordinated national management.

” In terms of the regulatory framework design of the future

cross-border carbon market, how to achieve a balance between

aligning with international standards to meet market expectations

and coordinating national management to safeguard national

interests, will become a recurring topic for both policymakers and

the market.

In recent years, there have been ongoing updates in sustainable

finance-related standards in the international market, some of

which have been incorporated into China’s policies and

standards, as appropriate. For example, on June 26, 2023, the

International Sustainability Standards Board (ISSB) issued the

final versions of two standards, i.e. IFRS Sustainability

Disclosure Standard: General Requirements for Disclosure of

Sustainability-related Financial Information (IFRS S1) and

IFRS Sustainability Disclosure Standard: Climate-related

Disclosure (IFRS S2), and the abovementioned ESG information

disclosure rules for listed companies controlled by central SOEs

and the private investment fund sector explicitly state that these

international standards will be taken into consideration. How to

better align international standards with China’s national

conditions, so as to integrate into the international market and

attract international investors within a safe and controllable

scope, will be a long-term issue for domestic policymakers.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link