Europe Sustainable Finance Market Size

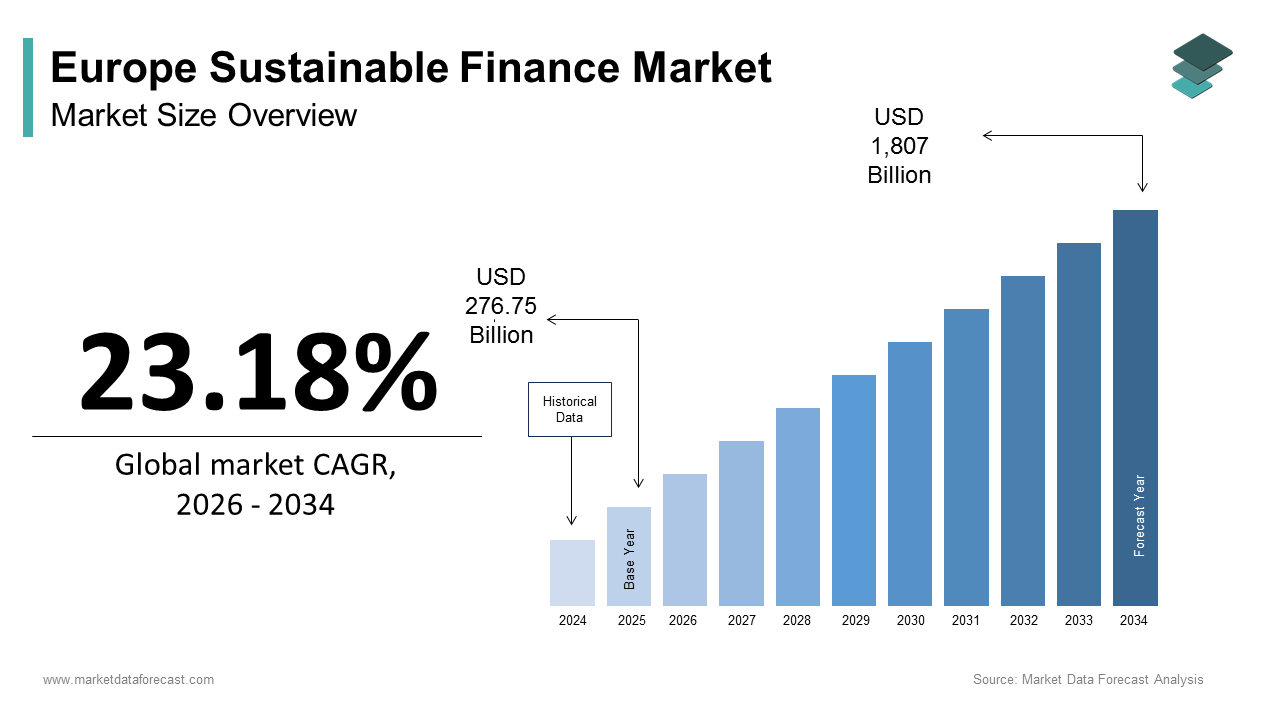

The Europe sustainable finance market size was calculated to be USD 276.75 billion in 2025 and is anticipated to be worth USD 1,807 billion by 2034, growing from USD 340.92 billion in 2026 at a CAGR of 23.18% during the forecast period.

Sustainable finance refers to the integration of environmental, social, and governance criteria into financial decision-making to redirect capital toward long-term ecological resilience and societal well-being. Unlike conventional finance, it embeds planetary boundaries and just transition principles into lending, investment, and risk assessment frameworks. The European Union has institutionalized this paradigm through binding regulatory architecture, including the Taxonomy Regulation, the Sustainable Finance Disclosure Regulation, and the Corporate Sustainability Reporting Directive. As per the European Commission, around 50000 companies across the EU are now required to disclose detailed sustainability performance data under the CSRD starting from 2025. Furthermore, the European Central Bank has already conducted a comprehensive climate-focused stress test across a wide range of significant institutions to evaluate their preparedness and the systemic risks related to climate change. According to sources, the European Union continues to work towards its ambitious climate neutrality goal, a target that experts and institutions suggest will require substantial, ongoing annual investment across various strategic sectors to bridge the funding gap. This systemic recalibration of capital allocation mechanisms positions Europe not merely as a market but as a regulatory laboratory for global sustainable finance standards.

MARKET DRIVERS

Mandatory ESG Disclosure Requirements Are Reshaping Capital Allocation Incentives

The enforcement of granular sustainability reporting obligations under the Corporate Sustainability Reporting Directive has fundamentally altered how financial institutions assess risk and opportunity, which drives the growth of the Europe sustainable finance market. A substantial number of European entities must now provide extensive sustainability disclosures, including all scopes of greenhouse gas emissions, under the Corporate Sustainability Reporting Directive. This data transparency enables asset managers to align portfolios with the EU Taxonomy’s technical screening criteria, which define what constitutes environmentally sustainable economic activity. European asset managers are increasingly integrating EU Taxonomy alignment metrics into their reporting, driven by regulatory obligations and growing market demand. The European Insurance and Occupational Pensions Authority observes a general increase in the number of insurers incorporating climate-related physical and transition risks into their overall risk and solvency assessments. These regulatory mandates reduce information asymmetry and create a level playing field where capital naturally flows toward verifiable sustainability performers rather than self-declared greenwashers. Consequently, demand for sustainable financial instruments, from green bonds to sustainability-linked loans, has shifted from voluntary preference to compliance-driven necessity.

Integration of Climate Risk Into Prudential Regulation Is Amplifying Institutional Demand

European financial supervisors have embedded climate considerations directly into capital adequacy and risk management frameworks, which propels the expansion of the Europe sustainable finance market. This compels banks and insurers to internalize long-term environmental externalities. In 2023, European authorities conducted simultaneous stress tests across a wide representation of the banking sector to assess resilience to economic and climate-related challenges. Recent European climate scenario analyses indicate that a sudden, disorderly shift to a green economy, combined with negative economic conditions, could lead to significantly elevated credit risk and increased potential losses in bank loan portfolios. As a result, the ECB now requires significant institutions to develop multiyear climate risk management plans as part of their Internal Capital Adequacy Assessment Process. Similarly, European regulatory bodies are consistently enhancing transparency requirements, mandating extensive annual public disclosures from banks regarding environmental, social, and governance (ESG) risks and the carbon footprint of their lending activities. The Network for Greening the Financial System has expanded to include a substantial majority of central banks and financial supervisors globally, including the European Central Bank and many national central banks across the European Union. This regulatory pressure cascades into client engagement as banks adjust credit pricing based on borrowers’ decarbonization trajectories. Major private financial institutions are increasingly implementing innovative financial products, such as sustainability-linked loans, which adjust lending rates based on borrowers achieving specific, independently verified environmental performance targets. This systemic recalibration ensures that sustainable finance is not a niche product but a foundational component of financial resilience.

MARKET RESTRAINTS

Persistent Data Fragmentation Undermines Comparable ESG Assessments

The region faces acute problems in data quality consistency and interoperability across sustainability metrics, despite ambitious disclosure mandates, which in turn impedes the growth of the Europe sustainable finance market. Investment fund documentation often displays a lack of uniformity in how environmental alignment is measured and reported. Variations in calculation methods can lead to differing sustainability profiles for funds with comparable investment objectives. Corporate reporting frequently lacks comprehensive, verified data regarding indirect emissions within the broader supply chain. A significant portion of a company’s environmental impact often stems from these indirect sources rather than direct operations. The absence of standardized disclosure practices complicates the ability of stakeholders to compare the ecological footprints of various market participants. This data gap forces financial institutions to rely on estimates, proxies, and third-party ratings that often lack transparency and exhibit low correlation. Mandated sustainability disclosures may just become a ‘box-ticking’ exercise without standardized digital reporting formats and public verification infrastructure, ultimately obscuring actual performance and eroding market integrity and investor trust.

Risk of Regulatory Arbitrage Due to Divergent National Implementation Timelines

The EU’s sustainable finance framework is in place, but its inconsistent adoption across member states is causing fragmentation and compliance uncertainty, which limits the expansion of the Europe sustainable finance market. European Union member states have consistently worked toward a unified, phased implementation of the Sustainable Finance Disclosure Regulation’s detailed disclosure requirements across the entire bloc. This discrepancy enables firms to relocate fund domiciliation or reporting functions to jurisdictions with lighter supervisory scrutiny. Additionally, non-EU financial centers like Switzerland and the United Kingdom are developing parallel but non-equivalent standards. The United Kingdom and the European Union have developed distinct approaches to classifying sustainable economic activities, resulting in a divergence in the scope of their respective green taxonomies. This regulatory asymmetry complicates cross-border capital flows and increases compliance costs for multinational asset managers who must maintain multiple reporting systems. Jurisdictional inconsistency will continue to partially constrain the single market for sustainable finance until the ESAs achieve supervisory convergence through binding technical standards and on-site inspections.

MARKET OPPORTUNITIES

Scaling Transition Finance for Hard-to-Abate Sectors Presents a Structural Opportunity

The region’s industrial decarbonization imperative has caused demand for transition finance mechanisms tailored to sectors where zero-emission technologies are not yet commercially viable, which provides new opportunities for the growth of the Europe sustainable finance market. Heavy industries have historically been underrepresented in sustainable financing relative to their emissions contribution. A new legislative framework in the region now explicitly supports industrial transition pathways, making them eligible for sustainability-linked financing instruments. Central banking institutions have started accepting transition bonds from heavy industry entities as collateral, provided these bonds align with specific, verifiable environmental targets. Industry groups project the potential mobilization of significant private capital for industrial transition projects, contingent upon the adoption of standardized performance indicators and verification protocols. This structured approach transforms high-carbon sectors from sustainability liabilities into investable transition opportunities, thereby expanding the market beyond renewable energy and electric mobility into the core of Europe’s industrial fabric.

Digital Infrastructure for Verifiable Impact Tracking Is Unlocking New Product Innovation

The emergence of secure digital platforms for real-time sustainability data exchange is enabling novel financial instruments with dynamic pricing linked to verified environmental outcomes, which is expected to fuel the expansion of the Europe sustainable finance market. Several countries are piloting digital registries that link corporate environmental reporting with financial systems to automate compliance. Industrial networks are connecting manufacturers and suppliers to share audited supply chain carbon data, which banks are using to adjust lending rates. Regulatory authorities have endorsed the use of distributed ledger technology for verifying the impact of green bonds, potentially reducing reliance on third-party attestations. Tokenized sustainability-linked bonds issued on regulated platforms have experienced significant growth, driven by demand for transparent impact attribution. This digital layer transforms sustainable finance from static label-based categorization to continuous performance-based capital allocation, thereby enhancing credibility, scalability, and investor confidence in measurable environmental returns.

MARKET CHALLENGES

Greenwashing Allegations Are Eroding Market Credibility and Consumer Trust

The proliferation of unsubstantiated sustainability claims continues to affect market integrity and deter mainstream capital participation, which challenges the growth of the Europe sustainable finance market. A significant number of reviewed product claims relating to environmental benefits have been found to lack clear substantiation or rely on general, non-standardized terminology. Moreover, a notable portion of investment funds marketed under the most stringent sustainability category have demonstrated limited alignment with established environmental criteria in initial portfolio evaluations. Discrepancies identified in the marketing and actual integration of environmental, social, and governance (ESG) practices have led to regulatory enforcement measures against specific asset managers. There is a developing trend of public caution, as recent surveys indicate that a minority of individual investors express confidence in the current labeling systems for sustainable investment funds. This credibility deficit increases due diligence costs for institutional allocators and discourages retail participation, and thereby constrains the market’s ability to achieve the scale necessary for systemic impact.

Talent Shortage in Interdisciplinary Sustainability Finance Expertise Is Constraining Implementation Capacity

There is a critical need for professionals with a versatile blend of financial acumen, climate science data analytics skills, and regulatory knowledge to successfully put the region’s sustainable finance framework into action, a shortfall which hinders the expansion of the Europe sustainable finance market. A notable pattern across the industry indicates that few financial institutions have established fully staffed departments dedicated solely to sustainable finance initiatives or the granular verification of alignment with common sustainability frameworks. Across many financial institutions, a perceived gap is consistently noted in the number of employees possessing the specific training needed to interpret complex environmental scenario data for credit assessment. There appears to be an observed lag in the development of dedicated, specialized academic programs within higher education to support the growing workforce demands in sustainable finance. This human capital bottleneck delays product development, increases reliance on external consultants, and heightens compliance risks as institutions struggle to interpret evolving technical standards from the Platform on Sustainable Finance. Europe’s ambitious sustainable finance goals risk outpacing actual capacity unless we invest together in reskilling and education reform.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

23.18% |

|

Segments Covered |

By Investment Type, Transaction Type, Industry Verticals, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

BlackRock Inc, Morgan Stanley, UBS Group AG, JPMorgan Chase & Co, Deutsche Bank AG, BNP Paribas, State Street Corporation, Goldman Sachs Group Inc, HSBC Holdings plc, ING Groep N.V., Allianz SE, Amundi, Triodos Bank, and Mirova |

SEGMENTAL ANALYSIS

By Investment Type Insights

The fixed income instruments segment dominated the Europe sustainable finance market by accounting for a 58.6% share in 2024. The dominance of the fixed income instruments segment is driven by the maturity, reliability, and regulatory alignment of green and sustainability-linked bonds. A notable preference exists among specific large-scale investors for fixed income instruments, driven by their stable and foreseeable cash flow characteristics and suitability for matching their long-term financial obligations. The inclusion of certain green bonds within a major central bank’s asset purchase initiatives has contributed to increased market depth and liquidity for these types of financial products. New regulatory measures establishing a regional standard for green bonds, which includes requirements for independent verification and specific alignment criteria, are strengthening investor confidence and mitigating concerns about misrepresentation of environmental claims. There has been substantial issuance of green bonds by regional entities, with the majority of proceeds directed toward financing renewable energy and energy efficiency projects that satisfy stringent technical criteria. This convergence of regulatory credibility, institutional demand, and transparent use of proceeds solidifies fixed income as the backbone of Europe’s sustainable capital markets.

The mixed allocation strategies segment is anticipated to witness the fastest CAGR of 18.7% from 2025 to 2033 due to investor demand for diversified sustainable portfolios that combine equities, fixed income, and alternative assets under unified ESG mandates. New sustainable investment funds are increasingly adopting diversified strategies that combine different asset types to manage risk while pursuing positive environmental or social impacts. This shift is being accelerated by the regulatory environment, which encourages managers to define and categorize products based on sustainability objectives. Consequently, a growing share of funds with high sustainability classifications are utilizing mixed-allocation strategies. Innovations in ESG data integration platforms enable real-time portfolio rebalancing based on corporate decarbonization progress, enhancing responsiveness. Mixed allocation is becoming the primary vehicle for mainstream retail investor adoption, which offers a way to gain comprehensive sustainability exposure while maintaining portfolio diversification.

By Transaction Type Insights

The green bonds segment led the Europe sustainable finance market by capturing a 42.5% share in 2024. The leading position of the green brands segment is attributed to standardized frameworks, strong sovereign issuance, and corporate climate commitments. There is a significant and growing volume of green bonds in circulation within the region. Public sector entities represent a substantial share of the total market volume. A key pattern is the allocation of proceeds from specific public bond programs exclusively to climate and biodiversity initiatives. The market shows a movement towards enhanced standards and increased transparency. The vast majority of regional green bonds currently meet advanced transparency benchmarks, a higher rate than typically seen in the global market. This regulatory rigor, combined with central bank eligibility and strong secondary market liquidity, has made green bonds the default instrument for institutional investors seeking verifiable environmental impact without compromising credit quality.

The ESG investing segment is likely to experience the fastest CAGR of 21.3% during the forecast period, owing to mandatory disclosures and the integration of sustainability into core investment processes rather than as a niche overlay. Following the implementation of the Sustainable Finance Disclosure Regulation (SFDR) Level 2 in the European Union in early 2023, an extensive majority of asset managers have incorporated ESG factors into their fundamental investment analysis processes. This shift moves beyond exclusionary screening toward active ownership, including voting on climate resolutions and engaging with portfolio companies on decarbonization roadmaps. The number of ESG-focused shareholder resolutions in Europe has increased significantly in recent years, demonstrating growing investor activism on sustainability issues. Furthermore, the European Commission’s MiFID II amendments require financial advisors to assess clients’ sustainability preferences during suitability tests, directly channeling retail capital into ESG-integrated products. Unlike labeled bonds, ESG investing permeates the entire capital allocation system, making it a structural rather than thematic driver of market evolution.

By Industry Verticals Insights

The utilities and power segment held the largest share of 36.6% of Europe sustainable finance market. The leading position of the utilities and power segment is credited to its direct alignment with decarbonization imperatives and regulatory certainty. A forward-looking pattern indicates a planned and substantial increase in the share of renewable sources in the total electricity generation mix. The pursuit of these targets necessitates considerable financial investment in both power generation facilities and the associated power infrastructure. Large energy providers are actively directing capital towards funding key sustainable projects, such as those related to wind and solar energy, as well as grid modernization. A common regional framework is being used to define and evaluate which specific activities and assets qualify as sustainable. Specific regulatory requirements mean that all new major infrastructure developments now include a formal review of their environmental impact. The combination of market activity and regulatory alignment is creating a structured system for developing fundable, sustainable assets. This combination of policy clarity, scalable project sizes, and verified environmental outcomes makes the power sector the natural anchor for Europe’s sustainable capital markets.

The transport and logistics segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 24.1% from 2025 to 2033. The rapid expansion of the transport and logistics segment is propelled by Europe’s aggressive vehicle electrification mandates and sustainable aviation fuel requirements. The adoption of electric vehicles across European markets has increased alongside expanded financial support for regional charging networks. New regulatory frameworks are encouraging the aviation industry to integrate sustainable fuels into its operations over the coming decades. Increased interest in biofuel production is being driven by long-term mandates for cleaner energy sources in the transport sector. Major logistics and shipping firms are utilizing specialized financial instruments to link corporate debt to environmental performance goals. Investment is being directed toward the development of innovative maritime vessels capable of running on alternative fuels. Sustainable transport has emerged as a primary focus for large-scale institutional financing compared to other economic sectors. Tighter EU CO2 emissions regulations for vehicles are accelerating the shift of investment capital into zero-emission logistics systems.

REGIONAL ANALYSIS

France Sustainable Finance Market Analysis

France outperformed other regions in the Europe sustainable finance market by accounting for a share of 22.6% in 2024. The dominance of the French market is driven by proactive sovereign issuance and a robust regulatory ecosystem. Public financial authorities have established substantial programs for issuing debt dedicated to environmental initiatives across a diverse range of ecological sectors. The domestic corporate market has experienced a significant shift toward sustainability-linked financing, reaching a higher level of integration compared to neighboring regional markets. National regulatory frameworks for climate risk transparency were implemented well in advance of broader international standards, establishing an early foundation for financial disclosure. Institutional collaboration through dedicated observatories facilitates the alignment of financial activities with environmental taxonomies and supports the growth of specialized technological innovation. Governance structures often include regular independent oversight to ensure that capital remains directed toward its intended environmental objectives. France’s leadership in hosting the IPSF secretariat extends its power from financial flows to setting worldwide standards, anchoring its pivotal role in Europe’s sustainable finance landscape.

Germany Sustainable Finance Market Analysis

Germany was the second-largest country in the Europe sustainable finance market by capturing a share of 19.9% in 2024. The growth of the German market is propelled by its industrial decarbonization financing needs and deep capital markets. There is a pattern of increased government-backed financial instruments for environmental projects and a trend among major corporations to link financing to environmental objectives. Regulatory oversight of ESG financial products has intensified, aiming for greater transparency and consistency, alongside a strategic allocation of public funds to reduce risk for private investment in challenging industrial sectors. This blend of sovereign leadership, industrial demand, and rigorous oversight positions Germany as a pivotal engine of market integrity and scale.

United Kingdom Sustainable Finance Market Analysis

The United Kingdom is also a key player in the Europe sustainable finance market, despite its departure from the EU, due to its globally influential financial center and early mover advantage in green finance. There has been a substantial accumulation of financial instruments dedicated to sustainable initiatives within the country’s financial market. Regulatory frameworks are evolving to require detailed classification and clear communication about the environmental credentials of financial products. The domestic regulations regarding sustainable disclosures, while comprehensive, are developing distinctly from those of neighboring regions. A prominent domestic exchange has emerged as a significant hub for listing debt instruments tied to sustainability. A significant volume of assets managed by retirement funds is now subject to mandatory evaluation and reporting concerning climate-related risks due to legislative obligations. This combination of market depth, regulatory ambition, and global connectivity ensures the UK remains a critical node in Europe’s sustainable finance network.

Netherlands Sustainable Finance Market Analysis

The Netherlands experienced a consistent growth of the Europe sustainable finance market owing to its leadership in sustainable banking and circular economy financing. Major Dutch financial institutions are increasingly integrating environmental and social criteria into their credit assessment processes for corporate clients. There is a growing movement within the banking sector to align large-scale lending portfolios with broad sustainability frameworks. Regulatory bodies are applying more rigorous standards to how financial products are categorized based on their environmental impact. Many investment funds that were previously labeled as having specific sustainable objectives have been adjusted to more accurately reflect their underlying assets. National financial strategies frequently involve the distribution of capital toward international projects focused on ecological transition. Financial instruments such as green bonds are being utilized to support infrastructure and development initiatives in various global regions. Amsterdam’s Green Capital Markets initiative also supports SME access to sustainability-linked loans through local guarantee schemes. The Hague serves as a hub for sustainable finance due to a concentrated ecosystem of impact investors, green fintechs, and multilateral institutions, establishing the Netherlands as a trusted conduit for domestic and cross-border capital.

Sweden Sustainable Finance Market Analysis

Sweden is anticipated to expand in the European sustainable finance market from 2025 to 2033 due to its integration of social and environmental objectives within a universal banking model. A significant amount of managed assets is directed into new equity and fixed income funds designated as promoting environmental or social characteristics, or having a sustainable investment objective. The national central bank has incorporated a climate-related assessment criterion into its corporate bond acquisition strategy, resulting in the exclusion of entities associated with substantial fossil fuel exposure. The nation’s electricity generation is predominantly derived from fossil-free sources, which helps facilitate the redirection of financial resources towards supporting a fair transition and initiatives focused on the preservation of biological diversity. Government-supported finance institutions are channeling a notable annual sum into infrastructure projects that are environmentally conscious and social housing programs. This holistic approach, blending climate neutrality, social equity, and financial innovation, positions Sweden as a benchmark for high ambition sustainable finance in Northern Europe.

COMPETITION OVERVIEW

Competition in the Europe sustainable finance market is defined by a race for regulatory credibility, technological differentiation, and impact integrity rather than price. Major banks, asset managers, and insurers compete by embedding sustainability into core financial infrastructure from loan covenants to index construction. The implementation of the Sustainable Finance Disclosure Regulation and EU Taxonomy has raised the bar for substantiation, reducing room for greenwashing and favoring institutions with robust data governance and third-party verification capabilities. Competition is further intensified by the convergence of finance, climate science, and digital innovation as firms develop proprietary scoring tools, real-time monitoring dashboards, and outcome-based instruments. While global players maintain a significant presence, European entities benefit from first mover advantage in regulatory interpretation and closer alignment with the EU’spolicy-drivenn market design. The market remains dynamic with collaboration through initiatives like the Glasgow Financial Alliance for Net Zero coexisting alongside fierce competition for mandates from institutional investors demanding both compliance and measurable impact.

KEY MARKET PLAYERS

A few major players of the Europe sustainable finance market include

- BlackRock Inc

- Morgan Stanley

- UBS Group AG

- JPMorgan Chase & Co

- Deutsche Bank AG

- BNP Paribas

- State Street Corporation

- Goldman Sachs Group Inc

- HSBC Holdings plc

- ING Groep N.V

- Allianz SE

- Amundi

- Triodos Bank

- Mirova

Top Strategies Used by the Key Market Participants

Key players in the Europe sustainable finance market deploy strategies centered on regulatory alignment through proactive participation in EU standard-setting bodies, development of proprietary ESG data, and impact verification platforms integration of climate and social metrics into core risk and pricing models issuance of innovative instruments such as biodiversity linked and just transition bonds and active stewardship including shareholder engagement and voting aligned with science based targets.

Leading Players in the Market

- BNP Paribas is a leading force in Europe’s sustainable finance market with extensive capabilities in green bond structuring, sustainability-linked loans, and ESG advisory services. The bank has played a pivotal role in developing the EU Taxonomy alignment methodology for corporate lending and actively co-chairs the UN Net Zero Banking Alliance’s European working group. The bank also launched a digital ESG data integration platform for institutional clients, enabling real-time portfolio alignment scoring against regulatory benchmarks. These initiatives reinforce its position as a solutions-oriented partner for corporates and asset managers navigating Europe’s complex sustainable finance landscape while influencing global standards through multilateral forums.

- Allianz Global Investors drives sustainable finance integration across Europe through its active ownership approach and taxonomy-aligned investment frameworks. The firm manages one of the continent’s largest Article 9 fund ranges and pioneered the use of climate scenario analysis in sovereign bond selection. AllianzGI also co-leads the EU Platform on Sustainable Finance’s sub-working group on social criteria, ensuring that European standards evolve beyond environmental silos. The firm advances global asset management by embedding sustainability into its core models, moving beyond mere overlays to deepen regulatory and client relevance in Europe.

- Legal & General Investment Management is a key architect of scalable, sustainable finance solutions in Europe with a strong emphasis on stewardship and real asset decarbonization. The firm has committed to net-zero aligned investments and developed one of the first heat decarbonization indices for UK social housing. It also co-founded the Climate Transition Finance Market Development Initiative, which brings together central banks, regulators, and asset owners to standardize transition finance disclosures. LGM connects finance with real-world green results in the EU by using data to prove impact and working with policymakers, making capital flow towards ecological and social good through measurement and advocacy.

RECENT HAPPENINGS IN THE MARKET

- On March 2,024 BNP Paribas launched a biodiversity-linked corporate loan framework in partnership with the French agricultural cooperative InVivo, enabling financing tied to verified species habitat restoration metrics across European farmland.

- In May 2024, Allianz Global Investors enhanced its ESG scoring system to include just transition indicators such as workforce retraining rates and community reinvestment plans,s aligning its European equity and bond portfolios with social dimensions of the EU Taxonomy.

- On February 20,24 Legal & General Investment Management founded the Climate Transition Finance Market Development Initiative with the Bank of England and major European insurers to establish standardized disclosure templates for transition-aligned investments.

- In November 2023, BNP Paribas introduced a digital EU Taxonomy alignment dashboard for corporate clients, allowing real-time tracking of economic activity eligibility and substantial contribution criteria across all financed emissions scopes.

- In September 2023, Allianz Global Investors integrated high-resolution satellite-based deforestation monitoring into its fixed-income research process to assess physical and transition risks in sovereign and commodity-linked bond portfolios across Europe and emerging markets.

MARKET SEGMENTATION

This research report on the Europe sustainable finance market has been segmented and sub-segmented based on investment type, transaction type, industry verticals, and region.

By Investment Type

- Equity

- Fixed Income

- Mixed Allocation

By Transaction Type

- Green Bonds

- Social Bonds

- Sustainability Bond

- ESG Investing

- Others

By Industry Verticals

- Utilities and Power

- Transport and Logistics

- Chemicals

- Food and Beverage

- Government

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link