Concentration transactions, including mergers, acquisitions, and the establishment of joint ventures that meet China’s turnover threshold, are subject to antitrust merger review. In recent years, driven by government industry policies, corporate consolidation in China’s financial industry has accelerated. Over the past four years, the State Administration for Market Regulation (“SAMR”), China’s antitrust authority, has reviewed more than 135 financial sector cases, nearly half of which involved foreign-to-foreign mergers.

In this article, we will introduce the competitive landscape of China’s financial industry (Chapter I), examine the policies driving consolidations within the industry (Chapter II) and key characteristics of SAMR-reviewed mergers (Chapter III), followed by industry outlook from the perspective of Chinese antitrust practitioners (Chapter IV).

For the purpose of the articles, we focus solely on mergers between institutions that have obtained administrative approval from financial regulatory authorities and hold financial licenses, such as banking financial institutions, securities firms, futures companies, insurance companies. Institutions like private equity funds, which only require registration and filing, are not included.

I. Market Development and Competitive Landscape in China’s Financial Industry

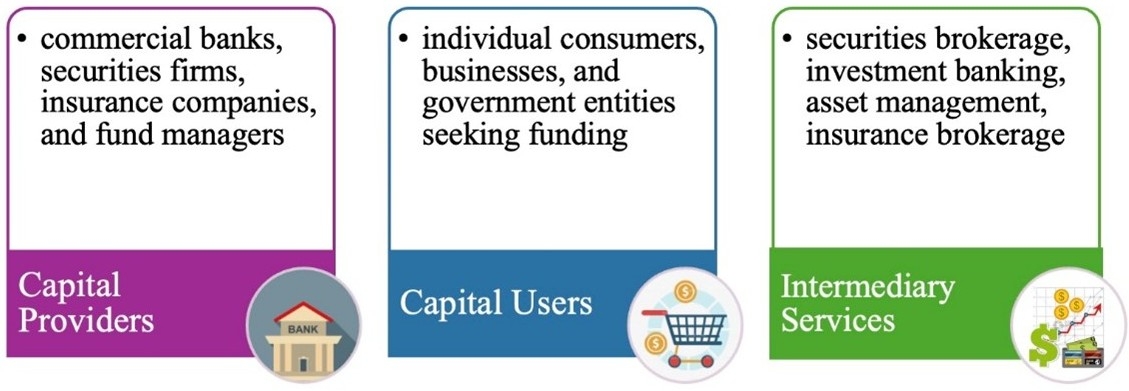

The financial industry consists of three main segments: on the supply side are banks, securities firms, insurance companies, and asset management firms, which channel funds into the market through deposits, bonds, and equity financing. On the demand side are individual consumers, businesses, and government entities seeking funding through loans, bond issues, and equity offerings. Intermediary services, such as securities brokerage, investment banking, asset management, and insurance brokerage, facilitating capital allocation and risk mitigation. Within this tripartite structure, banks hold a central position within China’s financial industry.

China’s financial industry has evolved into a highly competitive and structured landscape. In banking sector, competition is fierce and tiered, with the six major state-owned commercial banks, a range of national joint-stock banks, and various regional institutions (including city commercial banks and rural financial organizations) each hold unique positions in the market. Among these, state-owned banks maintain a significant market share (45%-50% in total, with the top bank holding around 10%) thanks to their scale and financial resources. Similarly, the securities industry is fiercely competitive, with leading firms like CITIC Securities leveraging their comprehensive strengths to secure top positions, each holding a market share of 5%-20%. However, overall market concentration in the sector remains relatively low.

Overall, competition in China’s financial industry is intensifying, placing increasing pressure on smaller institutions—such as local banks and smaller brokerage firms—which has led many to exit the market or merge with larger players. Meanwhile, high capital requirements, strict regulatory standards, and other barriers to entry have further solidified the competitive advantages of leading players.

II. Chinese Policies Initiative for Consolidations in the Financial Industry

Over the past few decades, China’s financial industry has undergone several significant waves of mergers and acquisitions, leading to industry concentration and consolidation.

The first wave (1995–2002), largely policy-driven, saw the financial industry transition from mixed to segregated operations. To mitigate the corruption and financial risks related to transactions with affiliates, a series of policies and regulation promoted the separation of different types of financial services, namely banking, securities, insurance, and trust. During this time, many securities divisions of banks were acquired by brokerage firms, leading to greater market concentration.

Subsequently, the second wave (2004-2006) was driven by operational risks within the industry, such as the misuse of client funds, prompting another round of regulatory intervention. High-risk brokerage firms were acquired—such as the 2005 acquisition of Southern Securities by Jianyin Investment—allowing leading brokerage firms to consolidate the market and spark the second wave of M&A activity.

The third wave (2008–2010) was prompted by regulatory policies like the “one holding, one participation” rule, aimed at addressing internal competition issues. During this period, major brokerage firms undertook strategic consolidation through share transfers or acquisitions, exemplified by China International Capital Corporation’s 2016 merger with China Investment Securities.

The fourth wave (2012–2020) involved market-driven acquisitions focused on enhancing competitiveness and pursuing global expansion, such as CITIC Securities’ acquisitions of Guangzhou Securities and Hong Kong’s CLSA.

In 2024, the Chinese government released new policies to foster consolidation in the Chinese financial industry. In March 2024, the China Securities Regulatory Commission (“CSRC”), the national authority overseeing the Chinese securities and futures markets, released Guidelines on Strengthening Supervision of Securities Companies and Public Funds to Accelerate the Development of World-Class Investment Banks and Asset Managers (“Guidelines”). This directive explicitly endorses M&A as a strategic tool for financial institutions to enhance competitiveness. The policy framework was further reinforced by the State Council’s updated Several Opinions on Strengthening Regulation, Preventing Risks, and Promoting High-Quality Development of the Capital Market in April 2024, which advocates for resource optimization through market-driven reorganizations. These regulatory tailwinds have catalyzed landmark transactions, including Guotai Junan Securities’ merger with Haitong Securities and Guosen Securities’ acquisition of Wanhe Securities.

Driven by these policy initiatives, the consolidation and restructuring of the financial industry is not only a natural outcome of market dynamics but also a key regulatory tool. As competition within financial markets intensifies and risk management requirements grow, the industry is expected to experience an even greater wave of consolidation in the coming years. Consequently, the scrutiny of concentrations in the financial industry will become more frequent.

III. Distinctive Features of Merger Control in China’s Financial Industry

Considering the above market trends, it’s important for undertakings to note merger control regulation which is a critical step in financial industry M&A transactions. Based on systematic analysis of 135 financial industry merger filings reviewed by SAMR from 2021 through July 2024, we identify several characteristics shaping antitrust scrutiny in this industry:

A. Prevalence of Simplified Review Procedures

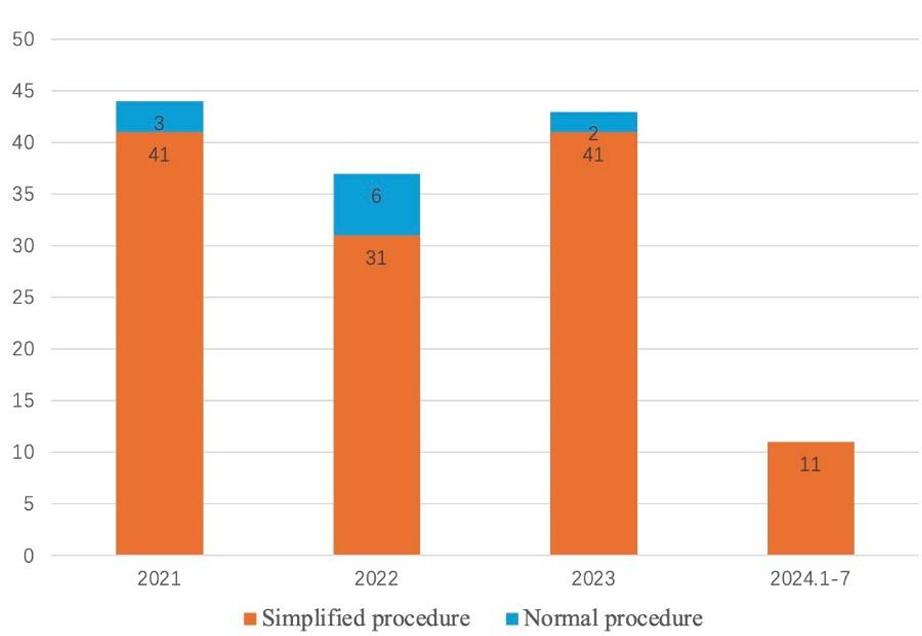

Between 2021 and July 2024, 135 merger review cases involving the financial industry were completed. Of these, 124 were reviewed under the simplified procedure, while 11 underwent the normal procedure. This mirrors the broader trend in China’s merger control practice, where simplified procedures dominate. Despite the significant influence of large players, China’s financial ecosystem remains structurally decentralized. For example, in the banking sector, large institutions hold dominant positions in terms of scale and service coverage, but regional and rural banks still play a critical role in the broader financial ecosystem.

While the pace of mergers and acquisitions in banking, insurance, and securities has picked up in recent years, the overall increase in industry concentration has been gradual. As market consolidation continues, however, the level of concentration is expected to rise steadily over time.

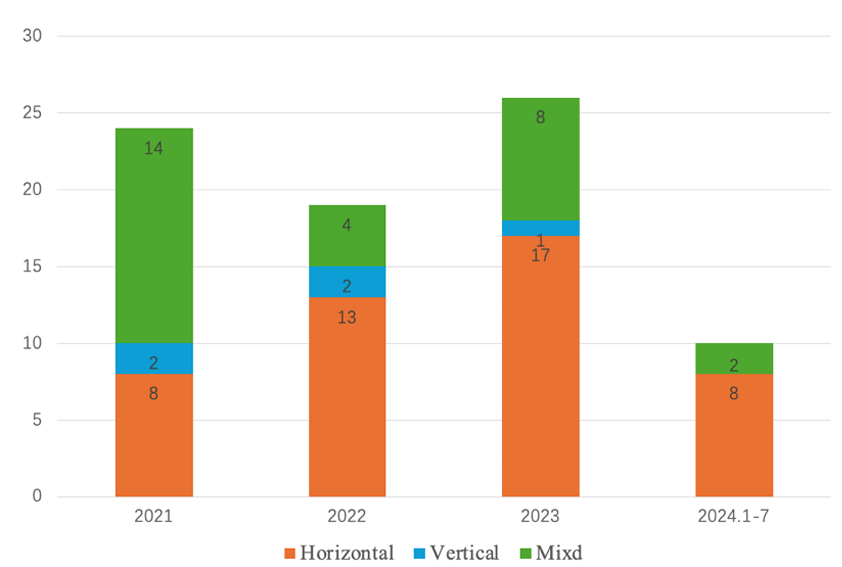

B. Horizontal Mergers Dominates Market Activity

A second key characteristic is that mergers in the financial industry are predominantly horizontal, involving businesses or products of a similar nature, while vertical integrations are relatively uncommon.

This structural preference stems from two key factors: First, the significant homogeneity of the industry—particularly in traditional banking and financial services—drives companies to pursue horizontal mergers in order to boost market share and enhance competitiveness. Second, under policies aimed at mitigating financial risks, fostering high-quality growth, and improving the overall health of the industry, many financial institutions have accelerated the disposal of non-performing assets and the optimization of their balance sheets, resulting in more horizontal merger activity. For example, in 2024 alone, over 180 small and medium-sized banks—mostly rural financial institutions—merged or exited the market. Intense market competition and regulatory measures have driven many smaller banks to exit or consolidate, making horizontal M&As the primary avenue for optimizing market structure and resource allocation.

In contrast, vertical integrations remain rare. This is largely because the financial industry’s supply chain is relatively simple, and most financial institutions focus on core financial products and services rather than managing complex supply chains such as those found in manufacturing. Consequently, the need for cross-industry or cross-business-chain vertical integrations is limited.

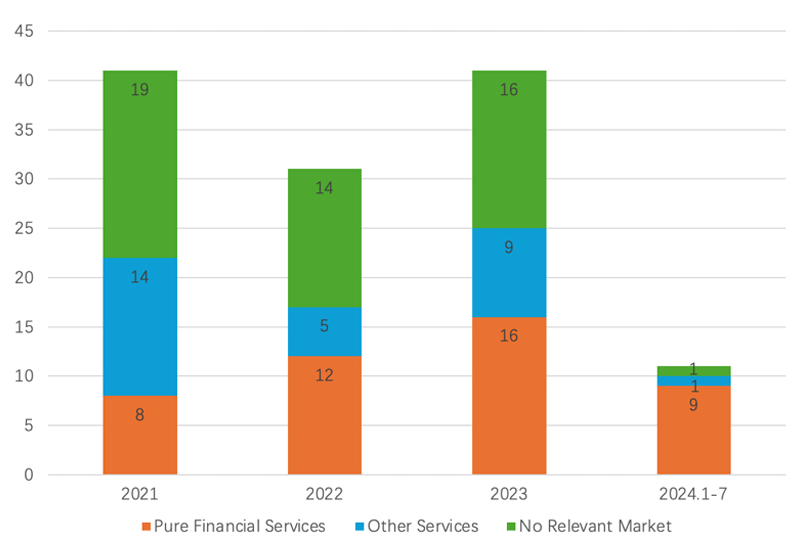

C. Mergers Focus on Intra-Industry Consolidation

A third key feature is that these cases mainly involve financial services, rather than other sectors, with most transactions closely tied to the target company’s core business. The majority of deals occur within specific financial sub-sectors, such as securities, insurance, banking, and asset management, reflecting a trend of intra-industry consolidation instead of cross-sector expansion.

This pattern highlights the growing competitive pressures within the financial industry. As competition intensifies, especially in areas like securities, mergers are becoming a vital strategy for undertakings to strengthen their market positions and adapt to changing market conditions.

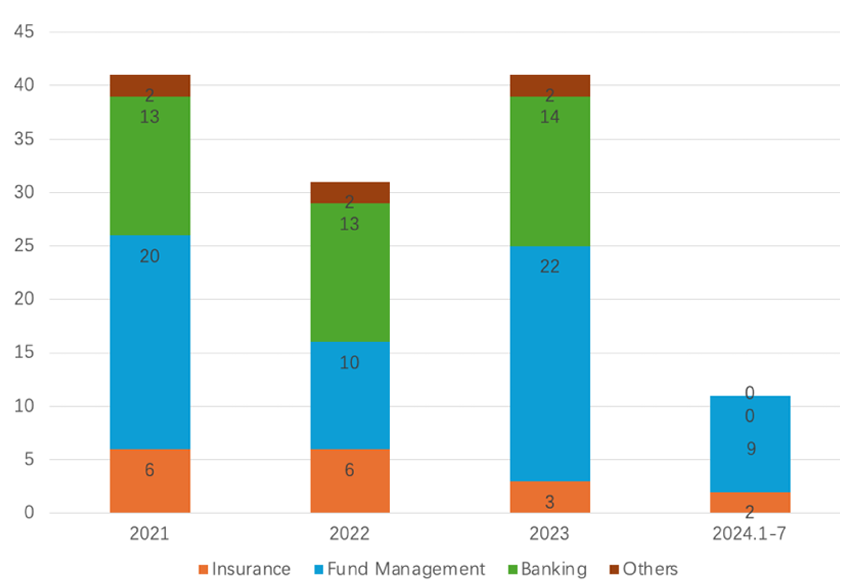

D. Active M&As in Fund Management and Banking Sector

Another trend is the active role of fund management firms in M&A activities, while activity in sectors like insurance remains relatively subdued. Meanwhile, bank mergers are on the rise, signaling two key developments: First, banks are playing a more active role in investment and capital operations, particularly in capital markets. Second, there is a increasing wave of consolidation within the banking sector, especially among smaller and regional banks. This highlights the ongoing restructuring and resource reallocation within the banking sector.

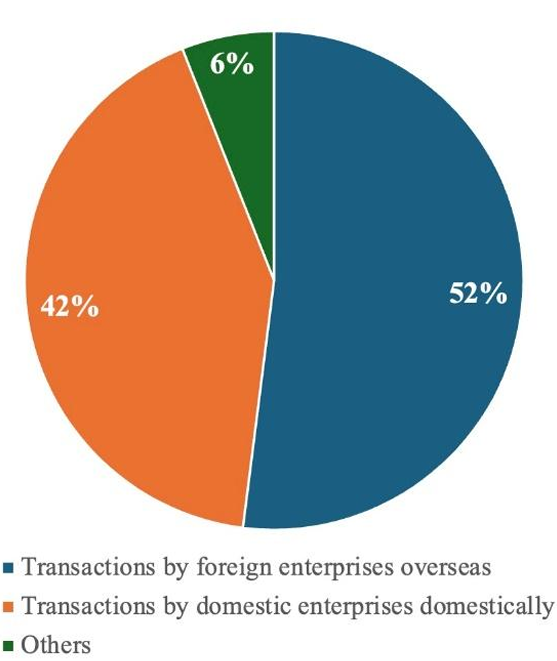

E. Limited Cross-Border M&As by China’s Domestic Firms

Another key trend is that Chinese companies largely focus their mergers and acquisitions on the domestic market, while most cross-border deals occur entirely offshore. These offshore transactions are often driven by foreign financial institutions pursuing global acquisitions, yet they still require notification under China’s merger control rules due to the potential impacts

on the Chinese market.

Within China’s financial industry, resource allocation and cross-border expansion remain conservative, with M&A strategies largely centered on integrating domestic resources and optimizing the local market structure. While some Chinese financial firms have started exploring cross-border acquisitions as part of their globalization strategies, the overall number and scale of these deals remain relatively small. Contributing factors include the still modest scale of China’s financial industry’s overseas ventures and the cautious approach prompted by strict financial regulations and cross-country policy disparities.

However, as China’s financial industry continues to open up—particularly under initiatives like the Belt and Road Initiative—the potential for cross-border M&A by Chinese financial firms is expected to grow. Additionally, domestic industrial upgrading and economic reforms are driving more financial institutions and fintech companies to expand overseas, aiming to meet the financial service demands of Chinese businesses operating abroad.

According to the CSRC’s March 2024 Guidelines, China aims to cultivate 2 to 3 globally competitive investment banks and asset managers by 2035. This long-term vision could further accelerate overseas acquisitions by Chinese financial firms, bolstering their global competitiveness.

IV. Outlook on Merger Control Trends in the China’s Financial Industry

In summary, although the overall concentration level of China’s financial markets remains relatively low, the pace of M&A within the industry is accelerating. Companies have been restructuring and reallocating resources in response to the intensified competition and regulatory initiatives, with mergers becoming a key strategy for growth and gaining a competitive edge.

Going forward, as regulations evolve and market conditions shift, the trend of industry consolidation is likely to deepen. Over time, the industry is expected to see greater concentration, more streamlined structures, and shifts in competitive dynamics. Additionally, although Chinese financial firms are still in the early stages of cross-border M&A, their role in global markets is set to grow. As these firms support the international expansion of Chinese businesses, their role in cross-border mergers will likely drive further market activity, both in China and abroad, potentially triggering the need to navigate complex merger control regulations.

At the same time, foreign companies must remain vigilant regarding China’s merger control rules. Foreign companies acquiring businesses in China—or conducting transactions abroad but has other business operations in China—must carefully assess whether filing thresholds are triggered. Under the amended Anti-Monopoly Law of China (2022), penalties for illegal concentrations have been significantly increased. The maximum fine for illegal concentration has been raised from RMB 0.5 million to up to 10% of the company’s previous year’s revenue, with particularly severe violations facing fines of two to five times that amount. “Gun-jumping” cases that do not have restrictive or exclusionary competitive effects can now incur fines of up to RMB 5 million. Several transactions have recently been penalized for such premature actions. As a result, financial institutions engaging in M&A need to consider not only the financial returns of the deal but also the necessity of merger control filings before closing, to avoid “gun-jumping” violations in China.

link